Group health insurance in 2025 is like your phone’s software update: inevitable, a bit pricey, and packed with features you didn’t know you needed—but can’t live without once you have them. Both employers and employees face rising costs, digital disruption, and changing expectations. Let’s dive in before your brain overheats faster than your Wi-Fi on a Zoom call.

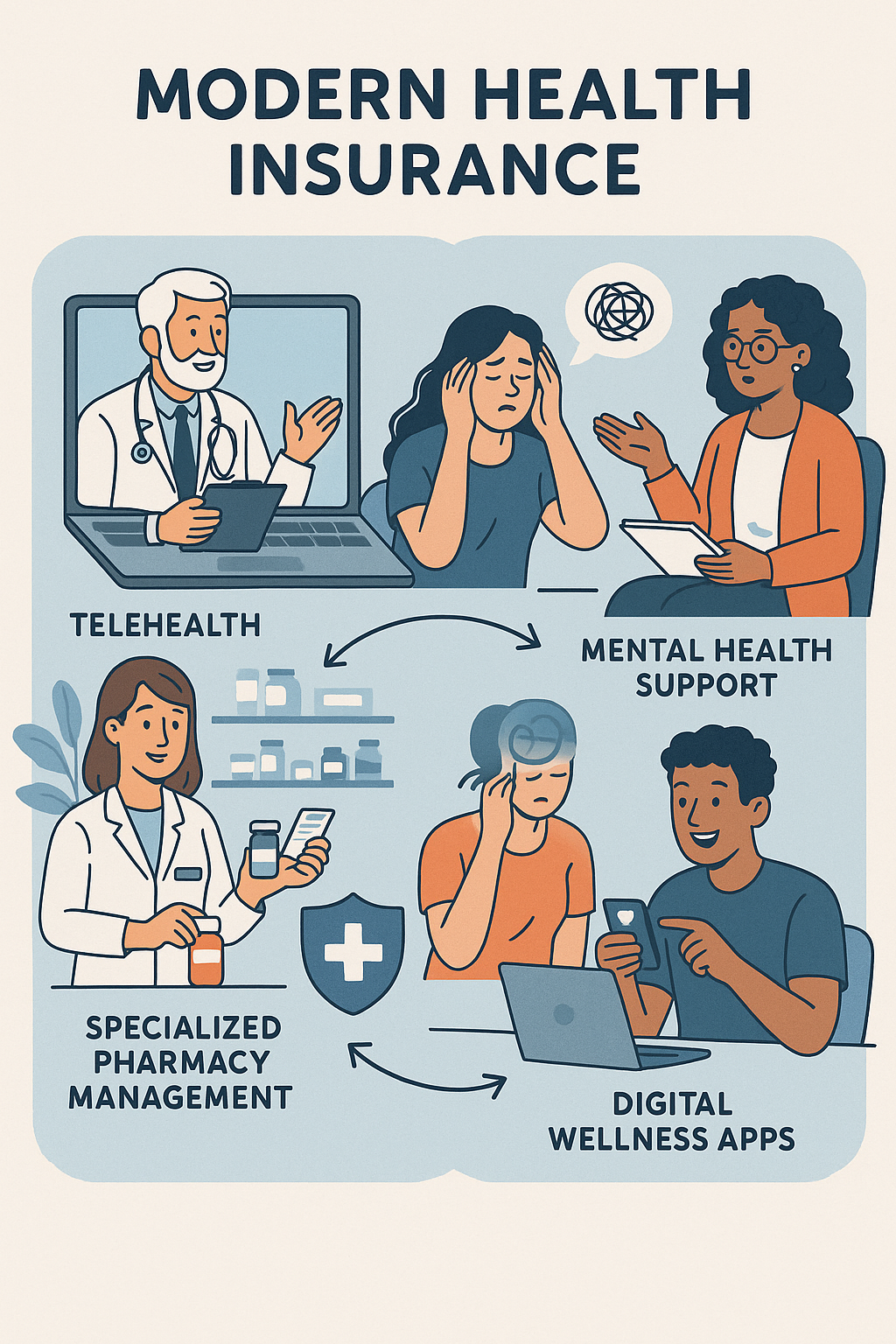

Health insurance premiums are climbing rapidly. Mercer reports over half of markets have trend rates above 10% for 2024–2025. Simply put, your benefits budget is bulking up, and employees want more than bandaids and aspirin. They look for mental health support, telehealth options, and personalized wellness apps — benefits that truly say “we see you.” Employers who master this balance gain big advantages in retaining talent and managing costs.

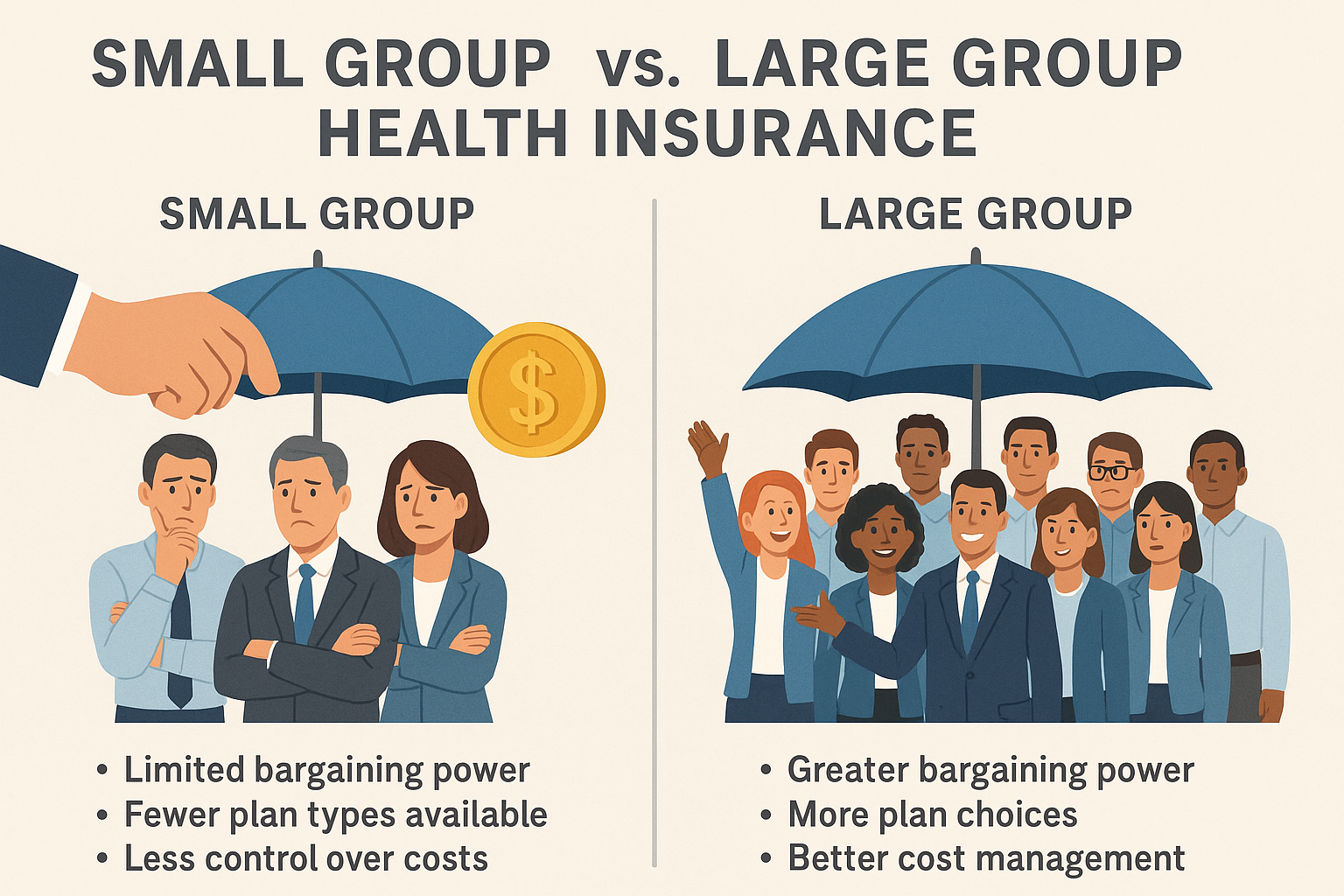

Consider your company size carefully when choosing your health insurance strategy.

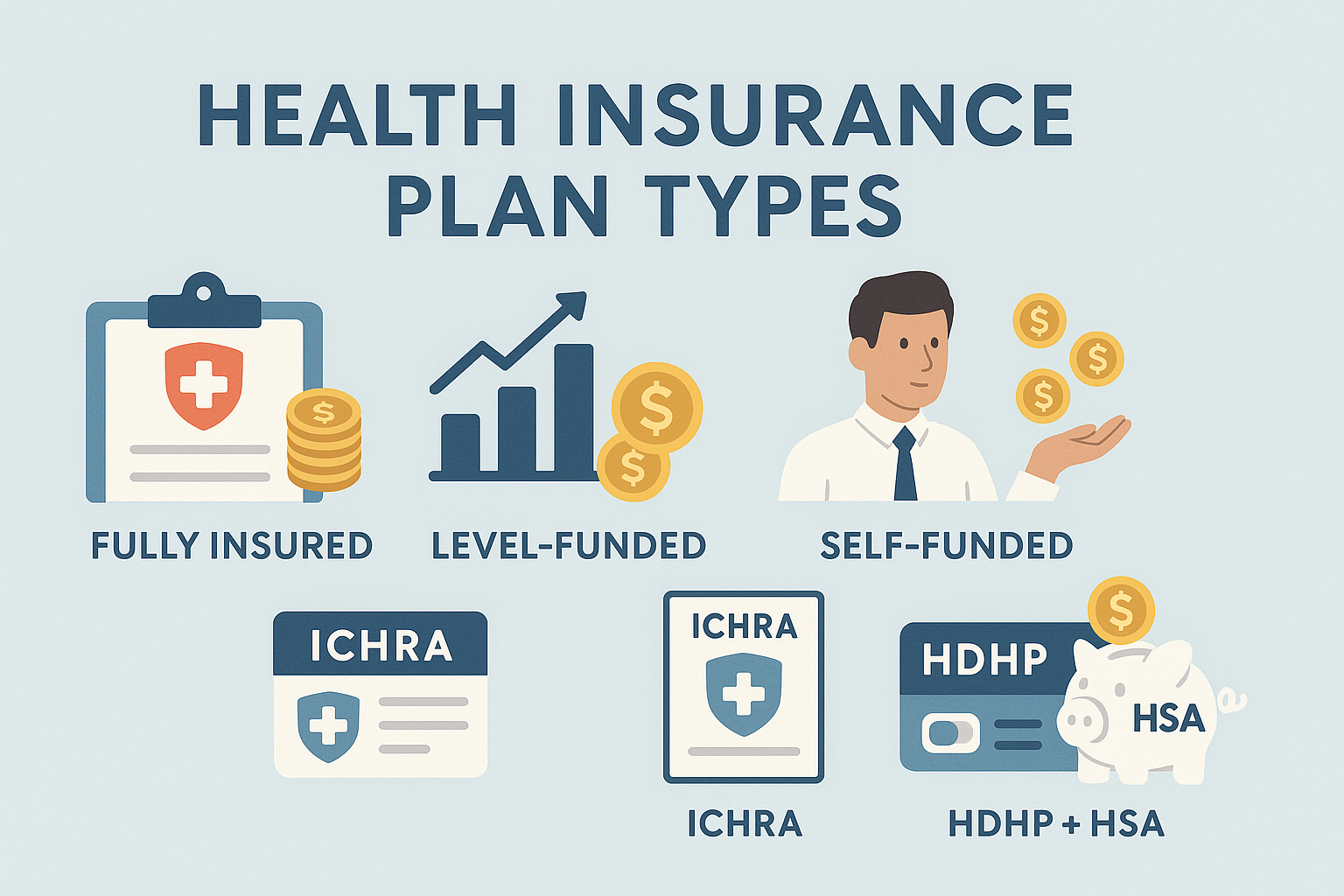

Choose your plan like you choose your coffee — based on your risk tolerance and needs.

Employers help cover premiums, and group risk pools reduce administrative costs per person. Custom benefits like mental health and telehealth meet workforce demands, and pre-tax perks reduce tax burdens. However, administrative complexity and the desire for portability and variety can challenge plans.

Companies using pharmacy management data curb specialty drug costs. Virtual-first plans reduce expensive in-person visits. Shifting from fully insured to level-funded plans brings budget stability and rebates. For example, a 120-employee manufacturer adopted level-funded coverage plus virtual care and diabetes management, flattening premiums and improving employee satisfaction.

ACA Marketplace offers flexibility and subsidies but less group tailoring. COBRA is an expensive short-term solution. Private group plans, especially level-funded and self-funded options, provide flexibility, control, and better cost management.

Group health insurance isn’t just a line item; it’s a strategic advantage. 2025 is already here, and employers who embrace flexibility, digital innovation, and empathy will win the talent battle and control costs. Need help? Reach out for templates, cheat sheets, and guides to make insurance approachable. Thanks for reading—you’re officially my favorite!